This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In total, EVOLVE welcomed attendees from more than 350 energy companies, including oil and gas operators, financial institutions, midstream firms, oilfield service providers and renewable energy developers. EVOLVE 2025 is more than a conference—it is a catalyst and full-fledged experience,” said Manuj Nikhanj, CEO of Enverus.

It was costing up to US$10/bbl to ship PW to out of state SWDs because Pennsylvania had only nine permitted SWDs. This led to a new midstream water industry developing almost overnight to treat and move PW around the shale play. The midstream water companies are behind this transition taking place so quickly.

These assets are pivotal to boosting black oil production to a projected 100,000–120,000 bbl/d. Strategic Focus: Infrastructure + Electrification = Value Creation Midstream Self-Sufficiency: BPX has built out its own gathering system, boosting reliability and flow assurance.

This bolt-on isn’t just about expanding land—it’s about unlocking 100+ gross operated two-mile locations with shallow declines and $30/bbl breakevens. The company sold midstream assets in Reeves County to Kinetik Holdings for $180 million, freeing up capital and sharpening its focus on core E&P operations.

While it lacks the scale of the Permian or Eagle Ford, the DJ offers operators attractive breakeven costs, strong midstream infrastructure, and a strategic position for gas-weighted growth. While not as prolific as the Permian or Eagle Ford, it offers strong midstream infrastructure and low breakeven costsmany sub-$50/bbl.

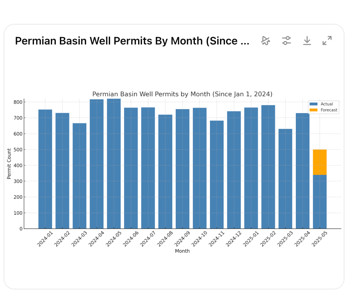

In early 2024, WTI crude prices averaged $77$80/bbl , whereas by Q2 2025, prices have softened to $60$70/bbl. Top 5 Operators by Well Permits in the Permian Oil Prices and Market Pressure Oil market fundamentals have shifted. Oil & Gas Account Directory Saskatchewan Light Oil Operator List Western Canada Heavy Oil Operator List St.

Competitive breakevens sub-$40/bbl support cash flow. Ring Energys facility acquisitions, revealed through TCEQ permit transfers, underscore its strategic expansion in Andrews County. As Chord Energy refocuses on the Williston Basin, Ring consolidates CBP assets to drive low-cost, margin-rich growth. Adds ~2,300 boe/d (80% oil) production.

share) at US$70/bbl WTI Free Funds Flow: $550 million Net Debt: Maintained under $1 billion with a 0.3x With a strategic focus on capital discipline, operational optimizations, and infrastructure enhancements, Whitecap is well-positioned to navigate commodity price volatility while delivering strong production growth and shareholder returns.

2025 Oil Production (bbl) Marathon Oil 641,000 EOG Resources 593,000 ExxonMobil (XTO Energy) 344,000 Crescent Energy (Javelin) 189,000 This move strengthens EOGs competitive positioning in an already active county and sets up the company for continued long-lateral drilling in one of North America’s most prolific shale plays.

The strategy focuses on: Capital discipline Optionality in completions Free cash flow preservation If oil prices fall below $55/bbl , SM may pause completions (the costliest phase), preserving capital while maintaining the ability to ramp up when market conditions improve. Month 2024 Actual 2025 Forecast June 4 7.4 August 16 6.3

oil production resilience depends on two pillars: An inventory of low-cost projects (sub-$40/bbl) Sustained operational activity to avoid decline and cost inflation Insights from the top oil & gas CEOs reinforce this modelbut they also reveal growing concern about capital discipline and production headwinds. Takeaway : U.S.

Sub-$40 Inventory Is a Strategic AdvantageIf You Use It Many top operators hold decades of drilling inventory with breakevens under $40/bbl. What industry leaders are saying about shale resilience, capital discipline, and the rise of AI-powered energy. oil and gas executives arent just reacting to the markettheyre actively redefining it.

Danny Wesson Through a lower share count, lower cost structure, and quality inventory, our breakeven oil price for the same free cash flow dropped $9/bbl from last year. Below, we unpack how top U.S. oil executives are framing the push for innovation and structural cost reductionand whether the momentum can last. The top U.S.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content