This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Denver-Julesburg (DJ) Basin continues to stand out as one of the most consolidated and cost-effective oil and gas plays in the U.S. Recent developments including record-setting drilling lengths, regulatory headwinds, and shifting capital strategies are reshaping how major and mid-sized players approach the basin in 2025.

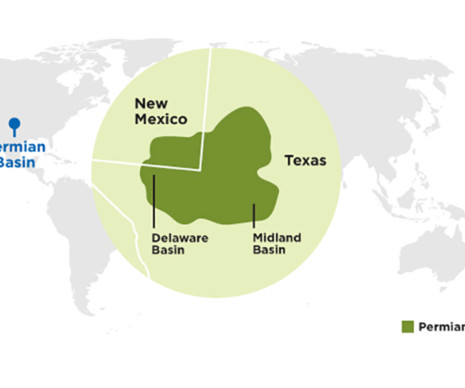

Over the past 15 years, the Permian Basin has transformed the landscape of U.S. million b/d ( 45% from 2020) Non-Permian Tight Oil (2024): 4.1 from 2020) Permian Plays Driving Production Permian Play 2024 Production Notes Wolfcamp 3.4 million b/d ( 45% from 2020) Non-Permian Tight Oil (2024): 4.1 crude oil production.

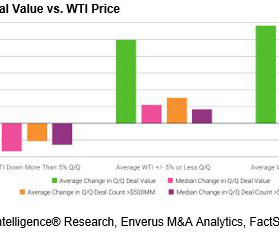

Upstream deal markets are heading into the most challenging conditions we have seen since the first half of 2020. Diamondback set a record in the Permian Basin with its acquisition of Double Eagle IV. On top of that, upstream companies will now have to navigate significant headwinds from falling oil and equity values.

In a strategic move aligned with shifting commodity price dynamics, SM Energy is proactively reducing its rig count in the Permian Basin through 2025. Taking them offline reflects a shift toward DUC (drilled but uncompleted) inventory building , a strategy SM effectively deployed during the 2020 downturn.

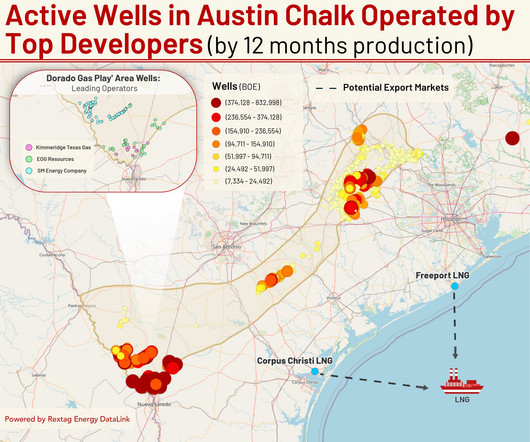

poised to expand LNG export capacity , interest in gassy basins has surged. Since 2020, Austin Chalk gas output has nearly tripled to 1.8 Bcf/d, while oil output from the formation has increased by 26,000 barrels per day ( bbl /d). According to the U.S. billion cubic feet per day (Bcf/d) in 2024 to 7.0 Bcf/d by 2026.

Andrew Dittmar, principal analyst at EIR, said that upstream deal markets are heading into the most challenging conditions his firm has seen since the first half of 2020. Diamondback set a record in the Permian Basin with its acquisition of Double Eagle IV.

poised to expand LNG export capacity , interest in gassy basins has surged. Since 2020, Austin Chalk gas output has nearly tripled to 1.8 Bcf/d, while oil output from the formation has increased by 26,000 barrels per day ( bbl /d). According to the U.S. billion cubic feet per day (Bcf/d) in 2024 to 7.0 Bcf/d by 2026.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content