Over the past 15 years, the Montney has solidified its position as Western Canada’s premier oil and gas play. The widespread adoption of horizontal drilling and multi-stage hydraulic fracturing around 2010 transformed it from a modest resource into a powerhouse, now producing over 2,000,000 boe/d. This output includes more than 10 BCF/d of natural gas volumes, complemented by substantial condensate, NGLs, and oil volumes, making the Montney the backbone of Canada’s ambitious LNG plans.

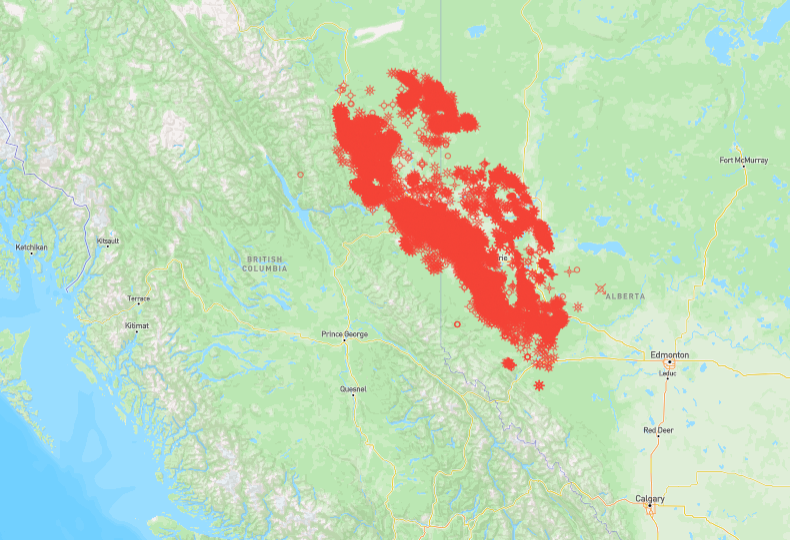

Figure 1 – Montney licences

However, low commodity prices are dampening activity in the Montney. Station 2 natural gas prices in British Columbia have remained weak for most of the past year, with Alberta’s AECO hub faring only slightly better. In contrast, U.S. pricing hubs like Henry Hub are buoyed by the country’s rise as the world’s largest LNG exporter. Adding to the challenge, a recent selloff in liquids prices and seasonal spring breakup conditions in Alberta and BC have further curtailed operations.

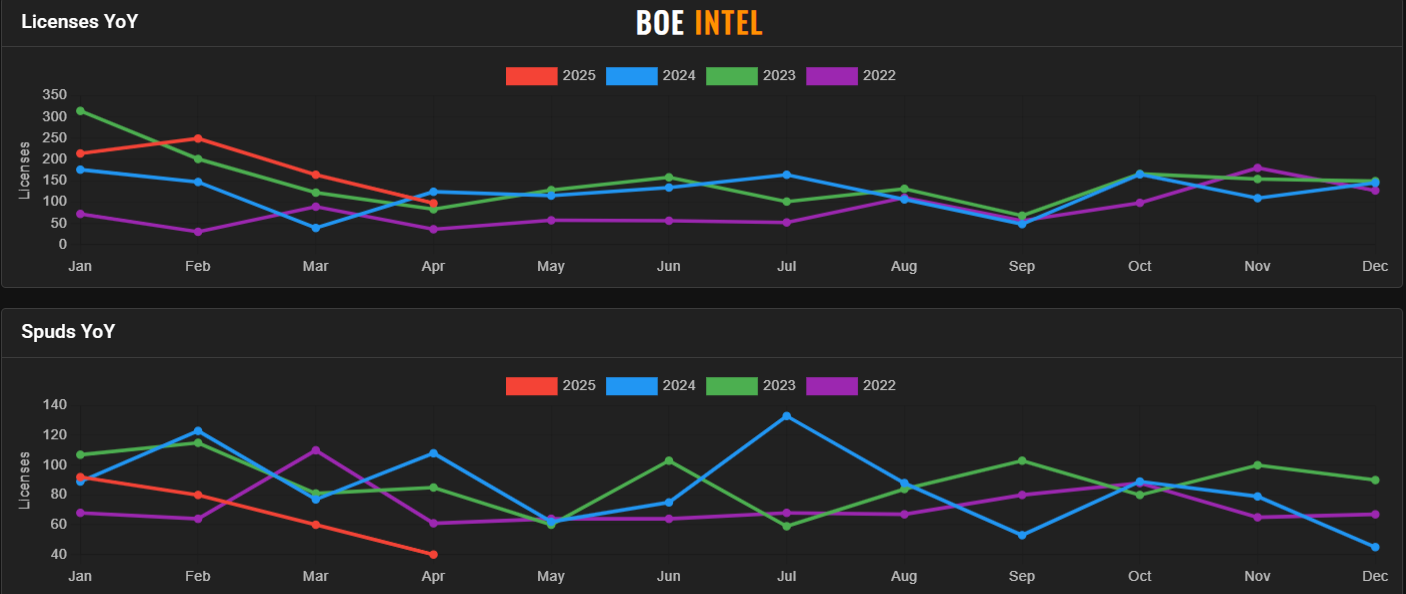

While licensing activity in 2025 has been robust—surpassing 2024 levels—spud activity has plummeted to multi-year lows (Figure 2). Operators are holding off on drilling, likely waiting for commodity prices to rebound rather than burn through inventory at low prices. Many are securing licenses now to be ready when LNG Canada ramps up demand for Montney gas. According to a recent Reuters article, that could be as soon as June.

The Montney’s vast resource scale ensures its long-term dominance, but near-term activity hinges on improved market conditions and the start of LNG exports.

Looking for access to BOE Intel charts, data, and more? Contact us here.

Figure 2 – Montney activity levels