This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The outlook for Western Canada’s heavy oil sector in 2025 is decisively optimistic. This upswing in permits aligns with broader capital plans from oil sands and thermal oil producers signaling renewed confidence in long-cycle heavy oil assets. Cost control, reliability Imperial Oil 400–430K ~2.0

Andrew McMurray, CEO of ShearFRAC, said, “Enverus was the obvious choice for us as a technology service business in the oil field services space. Collectively, these organizations represent: 60% of North American crude oil production 56% of natural gas production $12.1 Learn more at Enverus.com.

The Denver-Julesburg (DJ) Basin continues to stand out as one of the most consolidated and cost-effective oil and gas plays in the U.S. While it lacks the scale of the Permian or Eagle Ford, the DJ offers operators attractive breakeven costs, strong midstream infrastructure, and a strategic position for gas-weighted growth.

Canadas oil and gas sector remained resilient in 2024, with several operators reporting record-breaking production volumes. The data reflects both oil and gas output, offering a high-level look at market leaders, operational growth, and emerging trends in Canadian upstream development. 102,012 bbl/d (bitumen) SOR of 2.39

crude oil production. While legacy vertical well production has declined, horizontal drilling in tight oil plays, particularly in the Permian, has fueled unprecedented growth. Onshore Oil Production Trends (20102024) Metric 2010 2024 % Change Total Onshore L48 Production 3.4 million b/d 2.1 million b/d 8.9 million b/d ( 0.6

oil and gas executives arent just reacting to the markettheyre actively redefining it. Sub-$40 Inventory Is a Strategic AdvantageIf You Use It Many top operators hold decades of drilling inventory with breakevens under $40/bbl. oil & gas majors are now eyeing AI infrastructure as a growth vector. Its looking like [U.S.

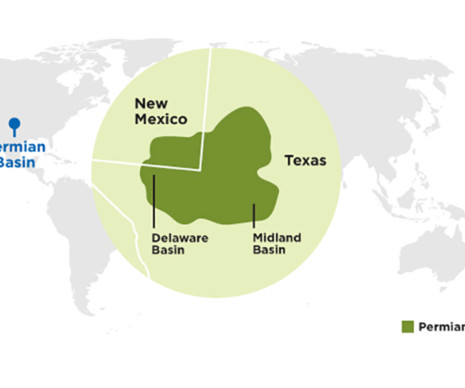

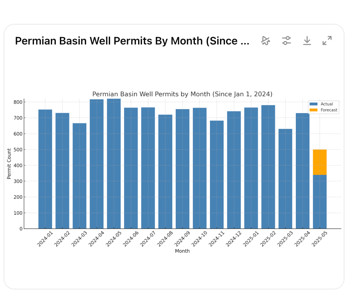

shale oil production, is experiencing a notable contraction in drilling permit activity this spring. Top 5 Operators by Well Permits in the Permian Oil Prices and Market Pressure Oil market fundamentals have shifted. In early 2024, WTI crude prices averaged $77$80/bbl , whereas by Q2 2025, prices have softened to $60$70/bbl.

oil production resilience depends on two pillars: An inventory of low-cost projects (sub-$40/bbl) Sustained operational activity to avoid decline and cost inflation Insights from the top oil & gas CEOs reinforce this modelbut they also reveal growing concern about capital discipline and production headwinds.

In todays lower-for-longer oil price environment, U.S. oil executives are framing the push for innovation and structural cost reductionand whether the momentum can last. Nick Olds, EVP Conclusion: Is $40 Oil the New Normal? shale operators must be relentless in their pursuit of cost efficiency. Below, we unpack how top U.S.

This reduction isnt reactionaryits part of a deliberate capital allocation strategy designed to protect margins and preserve flexibility in a potentially volatile oil market. Oil & Gas Account Directory Saskatchewan Light Oil Operator List Western Canada Heavy Oil Operator List St.

Ring’s acquisition of these mature assets aligns with its conventional oil growth model. Adds ~2,300 boe/d (80% oil) production. Competitive breakevens sub-$40/bbl support cash flow. Oil and Gas Account Directory Saskatchewan Light Oil Operator List Western Canada Heavy Oil Operator List St.

share) at US$70/bbl WTI Free Funds Flow: $550 million Net Debt: Maintained under $1 billion with a 0.3x Hedging Strategy for Downside Protection: 27% of 2025 oil production hedged at $102.17/bbl. Oil & Gas Marketing Lists Saskatchewan Light Oil Operator List Western Canada Heavy Oil Operator List St.

Trasko Development Potential: Long Laterals, Modest PDP The existing ASE South leaseproducing 2,0003,000 boe/d (85% oil)is expected to be a launching pad for longer wells. Oil & Gas Account Directory Saskatchewan Light Oil Operator List Western Canada Heavy Oil Operator List St.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content