This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

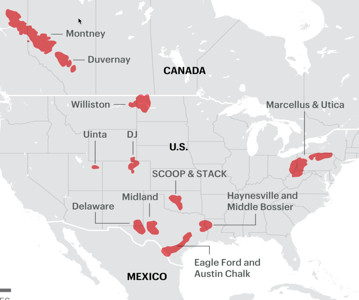

The report examines the effects on AECO hub gas pricing, the Canadian benchmark price for natural gas, from what is expected to be exceptional levels of condensate-directed Montney drilling in the coming years. This will result in substantial demand growth for in-basin condensate volumes because of increased need for diluent.

In a new white paper titled What Remains: North American Upstream Inventory, energy private equity firm Kimmeridge outlines which shale basins have the best runway for returns over the next 10 yearsand why the spotlight is now turning to Canada. Gas-Weighted Play: Strong economics tied to growing LNG demand and export potential.

Lets look at some of the key highlights: Anticipate a rise in oil production within the Western Canada Sedimentary Basin (WCSB). Explore the impact of increased oil sands production on the Canadian condensate and AECO gas markets. This could lead to an oversupply of cheap gas, putting downward pressure on AECO hub prices.

The company will gain exposure to both the liquids-rich and drygas windows, with firm transportation to premium marketsenhancing revenue predictability and price realizations. This deal now gives EOG three foundational plays: Delaware Basin, Eagle Ford, and Utica. Encino Acquisition appeared first on Oil Gas Leads.

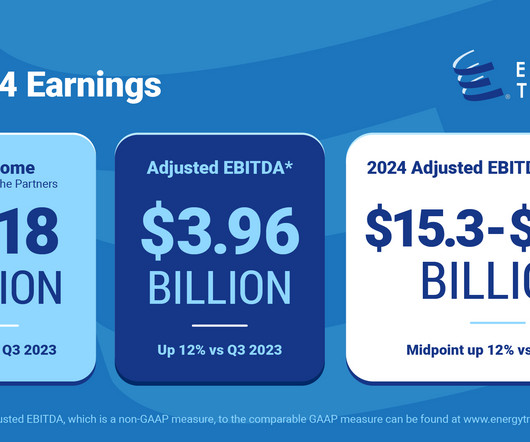

We also saw record performance in crude oil transportation volumes (up 25%), midstream gathered volumes (up 6%), NGLs produced (up 26%), and NGL fractionation volumes (up 12%) and transportation volumes (up 4%). This was offset by lower IT utilization in drygas areas due to the lower gas prices and weaker spreads.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content