This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Operator Strategies Reflect Growth and Efficiency Here’s a snapshot of what leading heavy oil players are planning in 2025: Company 2025 Production (bbl/d) 2025 CapEx (C$B) Strategic Focus Cenovus Energy 615–635K ~2.7–2.8 Optimization + brownfield growth CNRL 810–835K ~2.8 Maximize volumes, minimal downtime Suncor Energy 765–785K ~6.2

The Denver-Julesburg (DJ) Basin continues to stand out as one of the most consolidated and cost-effective oil and gas plays in the U.S. While it lacks the scale of the Permian or Eagle Ford, the DJ offers operators attractive breakeven costs, strong midstream infrastructure, and a strategic position for gas-weighted growth.

Over the past 15 years, the Permian Basin has transformed the landscape of U.S. 2020: Both Permian and non-Permian output dropped sharply due to WTI < $50/bbl and COVID-19. crude oil production. Onshore Oil Production Trends (20102024) Metric 2010 2024 % Change Total Onshore L48 Production 3.4 million b/d 2.1 million b/d 8.9

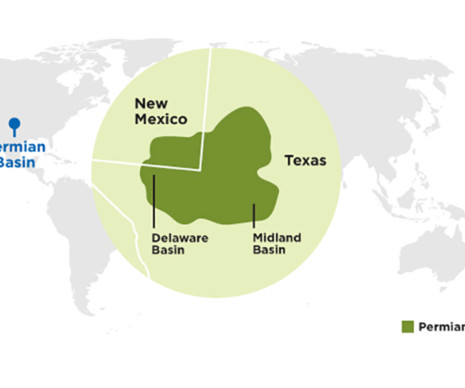

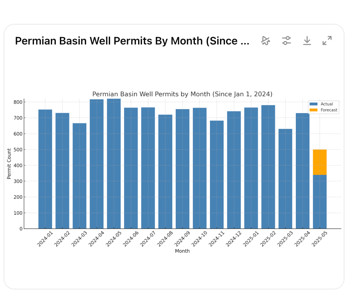

The Permian Basin, the beating heart of U.S. In early 2024, WTI crude prices averaged $77$80/bbl , whereas by Q2 2025, prices have softened to $60$70/bbl. shale oil production, is experiencing a notable contraction in drilling permit activity this spring.

As Chord Energy refocuses on the Williston Basin, Ring consolidates CBP assets to drive low-cost, margin-rich growth. These regulatory transfers aren’t just formalities theyre indicators of whos doubling down and whos cashing out in the Permian Basin. Competitive breakevens sub-$40/bbl support cash flow. Chord Energy).

102,012 bbl/d (bitumen) SOR of 2.39 147,819 BOE/d 69,827 bbl/d oil Smaller Producers (10,000 30,000 BOE/d) Company 2024 Average Production Notes Headwater Exploration 20,310 BOE/d +13% from 2023 Kiwetinohk Energy Corp. . ~580,000 BOE/d Includes 210,000 b/d oil and condensate Tourmaline Oil Corp. Vermilion Energy Inc.

In a strategic move aligned with shifting commodity price dynamics, SM Energy is proactively reducing its rig count in the Permian Basin through 2025. The company started the year with 9 active rigs , scaled back to 7 rigs by the end of Q1 , and plans to operate just 6 rigs for the remainder of the year.

2025 Oil Production (bbl) Marathon Oil 641,000 EOG Resources 593,000 ExxonMobil (XTO Energy) 344,000 Crescent Energy (Javelin) 189,000 This move strengthens EOGs competitive positioning in an already active county and sets up the company for continued long-lateral drilling in one of North America’s most prolific shale plays.

share) at US$70/bbl WTI Free Funds Flow: $550 million Net Debt: Maintained under $1 billion with a 0.3x With a strategic focus on capital discipline, operational optimizations, and infrastructure enhancements, Whitecap is well-positioned to navigate commodity price volatility while delivering strong production growth and shareholder returns.

oil production resilience depends on two pillars: An inventory of low-cost projects (sub-$40/bbl) Sustained operational activity to avoid decline and cost inflation Insights from the top oil & gas CEOs reinforce this modelbut they also reveal growing concern about capital discipline and production headwinds.

But as basins mature and geology becomes more challenging, the key question becomes: Can these gains be sustained, or has the industry already picked the low-hanging fruit? Travis Stice, CEO, Diamondback Technology and process efficiency gains are being outpaced by geology… its a natural evolution of a maturing basin.

Sub-$40 Inventory Is a Strategic AdvantageIf You Use It Many top operators hold decades of drilling inventory with breakevens under $40/bbl. Its looking like [U.S. production] peak could come sooner. Vicki Hollub, Occidental 2. But that advantage only matters if rigs stay active. Oil & Gas in 2025 appeared first on Oil Gas Leads.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content